There is no single answer to the question “is this person an employee or an independent contractor?” That’s not an evasion — it’s the uncomfortable legal reality. Three separate bodies of law, enforced by three separate authorities, each apply their own test to the same working relationship. A worker can be a legitimate contractor under IRS rules while simultaneously being an employee under their state’s ABC test. All three authorities can audit you. Independently.

Understanding how each test works — what it looks for, how it weighs different factors, and where the real risks lie — is not optional for any business that engages independent contractors. This guide breaks down all three frameworks in plain language.

Why There Is No Single Classification Standard

The fragmentation of US worker classification law is not an accident. It reflects the fact that employment classification serves different policy purposes in different legal contexts.

The IRS cares about classification because it determines who pays payroll taxes. When a worker is an employee, the employer withholds and remits income tax, Social Security, and Medicare. When a worker is a contractor, they are responsible for their own self-employment tax. The IRS wants to ensure that employers are not evading payroll tax obligations by calling employees contractors.

The Department of Labor cares about classification because it determines who receives the protections of the Fair Labor Standards Act — minimum wage, overtime pay, and child labor protections. The DOL wants to ensure that workers who are economically dependent on an employer are not denied FLSA protections through misclassification.

State labor authorities care about classification because it determines who receives unemployment insurance, workers’ compensation, state minimum wage and overtime protections, and — in some states — paid sick leave and other mandated benefits. States have a fiscal interest in ensuring that employers contribute to unemployment insurance funds for workers who will eventually claim benefits.

Because these authorities serve different purposes and have different enforcement interests, they apply different tests — and their conclusions can differ for the same worker in the same role.

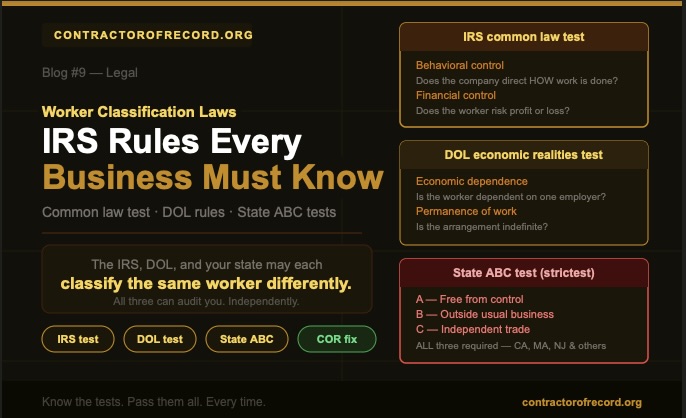

Framework 1: The IRS Common Law Test

The IRS Common Law Test is the oldest and most widely referenced classification standard in the US. It emerged from a line of federal court decisions and has been codified in IRS guidance as the primary framework for determining worker classification for federal tax purposes.

The test organizes relevant factors into three categories: behavioral control, financial control, and the type of relationship. No single factor is decisive; the IRS weighs the totality of the evidence.

Behavioral Control

Behavioral control factors examine whether the hiring party has the right to direct or control how the worker performs their work — not just what the end result will be. Key questions include:

Does the company provide detailed instructions about how, when, or where the work is to be done? Specific instructions about the sequence of tasks, the tools to use, or the hours to work suggest employment. General guidelines about the deliverable suggest contracting.

Does the company provide training to the worker? When a business trains a worker in the company’s specific methods and procedures, it indicates that the business wants the work done in a particular way — an employment indicator. Contractors typically bring their own skills and methods.

Does the company direct where the work is performed? Requiring a contractor to work from the company’s premises — particularly when the work could reasonably be done elsewhere — suggests control over work performance.

Does the company evaluate the process or just the result? Employers evaluate both how work is done and what is produced. Businesses engaging genuine contractors typically care about the deliverable, not the method.

Financial Control

Financial control factors examine whether the business controls the economic aspects of the worker’s job. Key questions include:

Does the worker have a significant investment in their own equipment, tools, or materials? A contractor who owns their own professional tools and infrastructure is operating an independent business. A worker who relies entirely on the hiring company’s equipment is more likely an employee.

Does the worker make their services available to the general market? A genuine independent contractor markets their services and has or seeks multiple clients. A worker whose entire professional identity is tied to a single company is economically dependent in a way that suggests employment.

Does the worker have the opportunity for profit or loss? An independent contractor who prices their work, manages their costs, and can make or lose money on a project is taking entrepreneurial risk. An employee receives a predictable wage regardless of business outcomes.

How is the worker paid? Payment by the hour, week, or month — particularly at a guaranteed rate — suggests employment. Payment by the project or based on deliverable completion suggests contracting.

Type of Relationship

Type-of-relationship factors examine the overall character of the working arrangement. Key questions include:

Is there a written contract that describes the relationship as contracting? A written contract is relevant evidence, but it is not determinative. If the economic reality of the relationship contradicts the contract, the IRS will look through the contract to the substance.

Does the company provide the worker with employee-type benefits? Health insurance, retirement contributions, paid vacation, and sick leave are indicators of employment. Contractors typically receive no such benefits.

Is the relationship permanent or indefinite? An engagement with a specific end date or project scope suggests contracting. An indefinite, ongoing engagement that continues as long as both parties wish suggests employment.

Is the work performed a key aspect of the company’s core business? When a company’s core business relies on the work of “contractors” — a software company whose product is built by “contractor” developers, a staffing company whose revenue is generated by “contractor” workers — classification risk is elevated.

How the IRS Weighs These Factors

The IRS does not apply a point system. A worker is not automatically an employee because more factors point that way than contractor factors. Some factors carry more weight than others based on the context.

The most critical factor in most modern classification disputes is the degree to which the company controls the manner and means of the worker’s performance — not just the result. A company that tells a worker what to produce is managing a contractor relationship. A company that tells a worker how, when, and where to work every day is managing an employment relationship.

If you are ever uncertain about a classification, filing IRS Form SS-8 requests a formal IRS determination. Be aware that this process can take over a year and may attract more scrutiny than you want — it is best used when you genuinely need certainty, not as a routine compliance tool.

Framework 2: The DOL Economic Realities Test

The Department of Labor applies the Economic Realities Test to determine classification under the Fair Labor Standards Act. This test takes a different philosophical approach from the IRS Common Law Test — instead of asking whether the company controls the worker, it asks whether the worker is economically dependent on the company.

In January 2024, the DOL finalized a new rule on independent contractor classification that reinstated the multi-factor economic realities analysis and rejected the prior administration’s two-factor approach. The 2024 rule is meaningfully stricter than its predecessor and has reclassified many workers who were previously treated as contractors.

The six core factors of the 2024 DOL economic realities test are:

Opportunity for profit or loss depending on managerial skill. Does the worker exercise managerial judgment — setting prices, negotiating contracts, deciding whether to take on a job — that affects whether they make or lose money? A worker who has no ability to influence their income through business decisions is more employee-like.

Investments by the worker and the potential employer. Does the worker make investments in equipment, tools, facilities, or workforce that are consistent with operating an independent business? Investment in productive capacity is a hallmark of genuine entrepreneurship. A worker whose “investment” consists only of a personal laptop is not making the kind of capital commitment that characterizes an independent business.

Degree of permanence of the work relationship. Is the relationship indefinite or continuous, or is it defined by a specific project scope or duration? Permanent or indefinite relationships resemble employment. Project-specific or occasional relationships resemble genuine contracting.

Nature and degree of control. This is conceptually similar to the IRS behavioral control analysis but also encompasses economic control — does the company set the worker’s rate, restrict their ability to work for competitors, or control other conditions of economic significance?

The extent to which the work performed is an integral part of the potential employer’s business. When work is central to the hiring company’s core function — not peripheral or ancillary — the worker performing that work is more likely to be economically integrated into the business in a way that resembles employment.

Skill and initiative. Does the worker bring specialized skills and apply them with independent business initiative? A worker who uses skills developed independently, markets those skills, and exercises business judgment in deploying them is more contractor-like than one who receives on-the-job training and follows company direction.

The 2024 DOL rule explicitly states that no single factor is determinative and that the totality of the circumstances governs. However, the rule gives additional weight to factors that most directly speak to economic dependence.

The Practical Impact of the 2024 DOL Rule

The 2024 rule has real consequences for businesses in several industries that historically relied heavily on contractor classifications — gig economy platforms, healthcare staffing, construction, trucking, and professional services. Workers who passed the prior administration’s two-factor test may no longer pass the six-factor economic realities analysis.

If your contractor workforce predates the 2024 rule change, this is a good time to conduct fresh classification reviews — not just based on historical practice, but based on the current regulatory standard.

Framework 3: State Classification Tests

State classification tests vary significantly, but the most consequential — and most employer-unfavorable — are the ABC tests now used by California, Massachusetts, New Jersey, Connecticut, Vermont, and several other states.

The ABC test creates a presumption of employment that the hiring party must rebut by satisfying all three prongs of the test. Failure to satisfy any single prong results in a finding of employment — regardless of how well the worker scores on the IRS or DOL tests.

The Three Prongs of the ABC Test

Prong A — Free from control and direction: The worker must be free from the control and direction of the hiring entity in connection with the performance of the work, both under the contract and in fact. This is similar to the behavioral control analysis under the IRS test, but the “in fact” language means that actual practice governs, not just what the contract says.

Prong B — Outside the usual course of business: The worker performs work that is outside the usual course of the hiring entity’s business. This prong is the one that catches the most businesses off guard. If a software company hires a software developer, that developer is performing work within the usual course of the company’s business and cannot be a contractor under Prong B — regardless of any other factors. If a law firm hires a plumber to fix its pipes, the plumber is outside the firm’s usual course of business and satisfies Prong B.

Prong C — Customarily engaged in an independently established trade: The worker is customarily engaged in an independently established trade, occupation, or business of the same nature as the work performed. The worker must actually operate an independent business — not just be theoretically willing to work for other clients.

Why the ABC Test Is So Consequential

Prong B makes the ABC test categorically more restrictive than both the IRS and DOL tests. A tech company that passes both federal tests with flying colors — because its developers have multiple clients, work independently, and take project-based engagements — will still fail Prong B in California if those developers are building software for the company, because software development is the company’s core business.

California’s AB5, passed in 2019, codified the ABC test for most California workers and triggered the most significant wave of contractor reclassifications in US history. The law has been amended multiple times — most significantly by AB2257 in 2020, which added exemptions for specific occupations — but its core requirements remain in force.

The following types of worker-business relationships are particularly high-risk in ABC test states: developers at tech companies, designers at design agencies, writers at media companies, drivers at transportation platforms, healthcare workers at staffing agencies, and construction workers at general contractors. In each case, the worker typically performs work that is integral to the company’s core function.

Other State Tests

States that have not adopted the ABC test generally apply some version of the IRS Common Law analysis, sometimes with additional factors. However, state enforcement intensity varies significantly — California, Massachusetts, New York, and Illinois are among the most actively enforcing states, while others are less aggressive.

New York applies a multi-factor test that weighs similar factors to the IRS analysis but has historically been applied broadly in industries like construction and media. Illinois applies an Economic Realities Test similar to the federal DOL standard for unemployment insurance purposes.

The Interaction Between Federal and State Tests

Here is the practical reality that creates the most risk for businesses: a worker can be classified differently under multiple frameworks simultaneously.

A developer working for a SaaS company might be a legitimate contractor under the IRS Common Law Test — they work independently, have their own tools, take project-based engagements, and have other clients. That same developer might be an employee under California’s ABC test — because software development is the company’s core business, failing Prong B. And they might be in a gray zone under the 2024 DOL Economic Realities Test — because the indefinite duration of the engagement and their economic dependence on the company weigh toward employment.

All three findings can coexist. The IRS may not challenge the classification while California’s Labor Commissioner actively investigates it. A compliance approach that focuses on passing one test while ignoring the others creates gaps that enforcement agencies exploit.

Practical Implications for Your Business

Applying all three frameworks to every contractor engagement is the correct approach — not just the IRS test, and not just the test of your home state.

For contractors in states with ABC tests, Prong B is the practical threshold question. If the contractor’s work is the same type of work that is central to your business, the ABC test almost certainly classifies them as an employee. This does not mean you cannot engage that worker — it means you need to structure the engagement carefully, potentially through an EOR rather than a COR, or with the guidance of a specialist.

For long-running, exclusive contractor relationships, both the IRS and DOL analyses are likely to find employment characteristics regardless of what state the contractor is in. Duration and exclusivity are among the most powerful indicators across all three frameworks.

Document your classification analysis in writing, applying each applicable framework, before every contractor engagement begins. If an audit ever occurs, documented good-faith analysis — even if the conclusion is later disagreed with — significantly reduces penalty exposure.

And for businesses operating across multiple states or internationally: the classification analysis must be conducted fresh for each jurisdiction. A worker who is clearly a contractor in Texas may be an employee in California. A worker who is clearly a contractor under US federal law may be an employee under German labor law.

How a Contractor of Record Helps

A Contractor of Record with genuine compliance expertise conducts multi-framework classification analysis as part of every engagement screening. The COR applies the IRS Common Law Test, the relevant DOL standard, and the classification framework of the contractor’s state or country — and documents the analysis.

If an engagement cannot pass all applicable tests as a contractor relationship, a legitimate COR will flag this rather than proceed. This is the most important quality signal when evaluating COR providers: a COR that will engage any worker regardless of classification risk is not providing compliance protection — it is providing payment processing while leaving your classification liability intact.